Explainable AI in finance exists to close a very specific, very consequential gap. Ask a loan officer from the 1990s why an application was rejected, and they could walk you through it: debt-to-income ratio too high, credit history too thin, collateral insufficient. Ask a modern gradient-boosted model or neural network the same question, and the honest answer is often “we don’t fully know.” That gap between decisions that affect real people’s mortgages, insurance premiums, and investment portfolios, and the inability to explain those decisions is exactly what explainable AI (XAI) in finance exists to close.

By mid-2026, this isn’t a theoretical debate anymore. The EU AI Act’s high-risk obligations, including explainability requirements for credit scoring and risk assessment systems, become fully enforceable on August 2, 2026. In the US, the Equal Credit Opportunity Act has quietly required lenders to give specific reasons for credit denials since 1974 AI doesn’t get a pass just because the model is more complex than a spreadsheet. And a fresh wrinkle has emerged this year: regulators are now openly admitting their guidance doesn’t cover the AI systems banks are actually deploying fastest.

What Explainable AI Actually Means in a Financial Context

Explainable AI is not one technique it’s a design goal. It refers to methods and practices that let a human understand, in terms they can act on, why a model produced a specific output. In finance, “understand” has to satisfy several very different audiences at once: a data scientist debugging a model, a compliance officer defending it to an examiner, a customer who wants to know why they were declined, and a board member deciding whether to trust it with capital allocation.

That multi-audience requirement is the part most introductory explainers skip past. A SHAP force plot that satisfies a model validator will mean nothing to a customer service rep on the phone with a declined applicant. Building XAI into a financial institution isn’t a single deliverable it’s closer to translation work, repeated for every stakeholder who has a legitimate reason to ask “why.”

The Core Techniques, and Where Each One Breaks Down

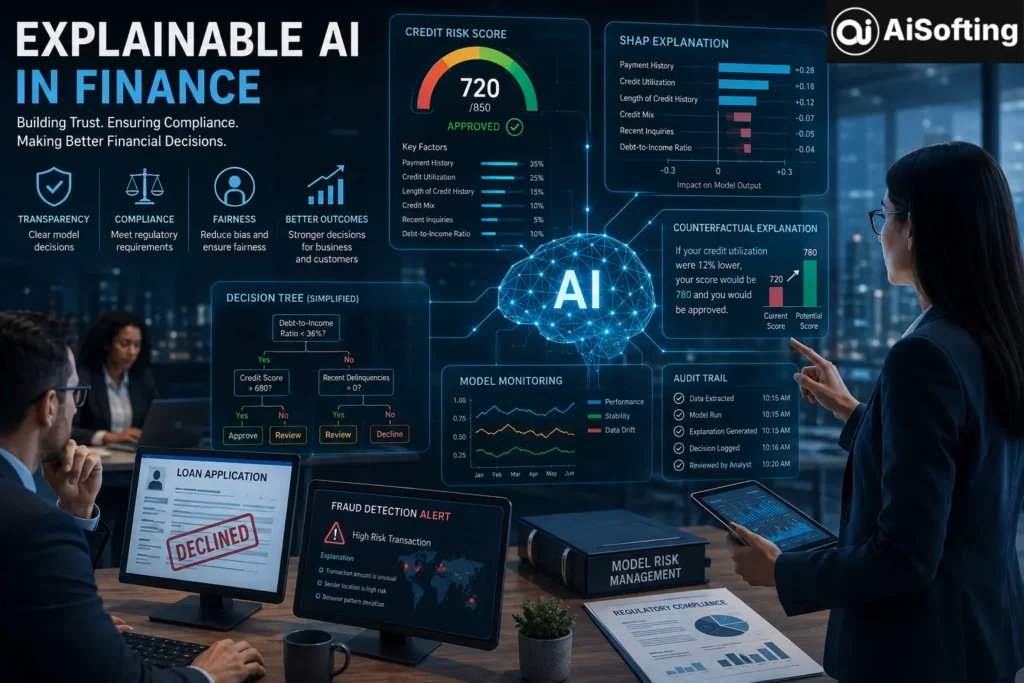

Two methods dominate practical deployments right now: SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-Agnostic Explanations). SHAP borrows from cooperative game theory to assign each input feature a consistent share of credit or blame for a prediction, which makes it useful for both individual-decision explanations and portfolio-wide analysis of what a model is really keying on. LIME instead builds a small, simple, interpretable model that approximates the black box’s behavior in the neighborhood of one specific prediction.

Recent comparative research on credit risk models is candid about the tradeoffs: SHAP tends to be more theoretically consistent but computationally heavier, while LIME is faster but can produce different explanations for the same prediction if you run it twice, which is a serious problem when a regulator asks you to reproduce an explanation months later. A 2026 study on bond default risk modeling went further, proposing a way to measure how much SHAP and LIME actually agree with each other as a proxy for how trustworthy either explanation is an implicit admission that neither method is ground truth on its own.

Counterfactual explanations “you would have been approved if your utilization ratio were 12% lower” have gained ground precisely because they answer the question customers actually ask, rather than the question data scientists find most tractable. They’re also easier to make compliant with adverse-action notice requirements than a raw feature-importance chart.

What most XAI content skips: none of these methods are appropriate for every model type by default, and organizations that bolt on SHAP as an afterthought without picking model architectures that suit their explainability strategy from the start tend to end up bottlenecked at validation.

The Regulatory Landscape Has Split Into Two Tracks

There’s a pattern in 2026 regulation that’s easy to miss if you only read headlines about “AI rules”: regulators are moving confidently on traditional, deterministic models and moving cautiously sometimes explicitly punting on generative and agentic AI.

Track one established models. The EU AI Act classifies credit scoring, lending decisions, and insurance risk assessment as high-risk applications requiring transparency, human oversight, and documented risk management, with enforcement starting August 2026. In the UK, the Financial Conduct Authority and Bank of England have chosen to police AI through existing frameworks rather than new AI-specific statutes, which in practice means firms are expected to justify AI decisions under rules that were written before anyone imagined a gradient-boosted ensemble making them.

Track two generative and agentic AI. This is where the real story is. The Federal Reserve, OCC, and FDIC’s April 2026 update to model risk management guidance (SR 26-2) explicitly excludes generative and agentic AI from its scope, describing the technology as “novel and rapidly evolving,” even while regulators simultaneously press banks on kill switches and vendor accountability in every standard exam. That’s a genuinely awkward position: the fastest-growing category of AI deployment in banking is the one with the least formal supervisory guidance. Institutions are left applying old principles to new architecture and hoping the interpretation holds up later.

This split matters because most explainability programs were built for track one static models with fixed inputs and outputs, where you can compute a SHAP value and file it. Agentic systems that plan, call tools, and take multi-step actions autonomously don’t produce a single decision you can attribute cleanly to input features. Explaining why a scorecard flagged a transaction is a solved problem. Explaining why an autonomous agent chose a sequence of five actions, several of which involved judgment calls, is not and it’s the problem the industry is walking into next.

Where Explainability Is Being Tested Hardest Right Now

Credit and lending. This remains the clearest legal battleground because adverse-action notice requirements predate AI by decades. Recent applied research combining SHAP-guided feature selection with LIME-based interpretability in loan approval systems shows the industry converging on hybrid approaches rather than picking one technique using SHAP for global feature ranking and LIME for individual applicant explanations.

Fraud and anti-money-laundering. Here the tension runs the other direction. Investigators want speed and few false positives; adding heavyweight explanation layers can slow detection just when speed matters most. Institutions are increasingly building explainability into the alert triage layer instead of the detection model itself, so investigators get a defensible rationale for the cases they escalate without throttling the model catching fraud in real time.

Agentic compliance workflows. Several banks, including early deployments involving Anthropic’s agent infrastructure at institutions like BMO and Amalgamated Bank, have focused less on explaining a single model output and more on making every step an agent takes traceable and auditable logging the tools it called, the data it read, and the reasoning path, so a human can reconstruct the “why” after the fact even without a single clean feature-attribution number.

The Underrated Problem: Explanation Overload

Nearly every vendor guide talks about the risk of too little explainability. Fewer talk about the opposite failure mode, which shows up constantly in practice: giving stakeholders more explanation than they can use. A risk officer handed a raw SHAP summary plot with forty features often can’t extract an actionable insight any faster than they could from a black box they just have more numbers to not understand. Teams frequently report that staff lack the skills to act on the explanations they’re handed, so misinterpretation replaces black-box opacity with a different kind of confusion.

The fix isn’t more explanation it’s tiered explanation. A technical audience gets the full feature-attribution breakdown. A compliance reviewer gets a plain-language summary mapped to specific regulatory criteria. A customer gets one or two concrete, actionable reasons. Building three interfaces to the same underlying explanation is more work than most roadmaps budget for, and it’s the single biggest reason XAI initiatives stall after the proof-of-concept stage.

My Experience with Explainable AI in Finance

Working through XAI implementations with financial teams reviewing model documentation, sitting in on validation discussions, and reading post-mortems from institutions that got this wrong a few patterns show up again and again that don’t make it into vendor pitch decks.

The first is that explainability projects almost always start as a compliance checkbox and only later get recognized as a genuine business advantage. Teams initially resent the extra engineering work, then discover that being able to explain a model’s behavior makes debugging it dramatically faster too an unexpected feature attribution often surfaces a data leakage problem or a proxy variable acting as an illegal discrimination signal long before it would have shown up in an audit.

The second pattern is more sobering: the gap between having an explainability tool and having an explainability practice is enormous. It’s not hard to install SHAP. It is hard to get a credit committee to actually change a lending policy based on what SHAP reveals, especially when the finding is uncomfortable for instance, that a model is leaning heavily on a variable correlated with a protected class even though that variable was never explicitly included. Institutions that treat explainability as a report to file are missing the point; the ones that treat it as an early-warning system for bias and model drift get far more value out of the same underlying math.

Third, the agentic AI transition is catching almost everyone flat-footed, and it’s worth saying plainly: most of the explainability tooling built over the last five years assumes a model that takes an input and returns an output. Multi-step, tool-using agents break that assumption, and organizations rushing agentic deployments into production without first solving traceability are building a documentation debt they’ll be paying down under regulatory pressure within the next year or two.

Finally, the honest caveat: XAI methods themselves have real limitations. SHAP and LIME can disagree with each other on the same prediction, and neither is a certified ground truth about what a model “really” did they’re approximations. Treating an explanation as unquestionable is its own risk.

Practical Recommendations

- Choose model architecture with explainability in mind from the start rather than retrofitting explanation methods onto a model already in production.

- Build tiered explanations for different audiences instead of a single technical output everyone is expected to interpret.

- Extend model risk management practices to generative and agentic AI now, even though formal supervisory guidance in the US currently excludes them regulators have made clear that existing risk principles still apply in spirit.

- Treat explanation disagreement (e.g., SHAP vs. LIME diverging) as a signal worth investigating, not noise to average away.

- Train the humans who receive explanations, not just the engineers who produce them an explanation nobody can act on isn’t meeting the actual goal.

Frequently Asked Questions

What is explainable AI (XAI) in finance?

It’s the set of techniques and practices that make an AI model’s decisions understandable to humans regulators, auditors, and customers rather than leaving the reasoning locked inside an opaque model.

Is explainable AI legally required for banks?

In the EU, yes for high-risk uses like credit scoring, with the AI Act’s obligations fully applying from August 2, 2026. In the US, there’s no single comprehensive AI law, but the Equal Credit Opportunity Act already requires specific reasons for credit denials, and banking regulators are actively examining AI governance during routine audits.

What’s the difference between SHAP and LIME?

SHAP assigns each feature a mathematically consistent contribution to a prediction based on game theory, useful for both individual and model-wide analysis. LIME builds a simplified local model around one specific prediction; it’s faster but can be less stable across repeated runs.

Does explainability slow down AI models?

It can add computational and engineering overhead, particularly for real-time use cases like fraud detection. Many institutions handle this by applying heavier explanation methods only at the point where a human reviews an alert, rather than at the detection stage itself.

Is agentic AI covered by the same explainability rules as traditional credit models?

Not yet, in most jurisdictions. US banking regulators’ 2026 model risk guidance explicitly excludes generative and agentic AI from formal scope while stating that existing risk principles still apply leaving institutions to build their own governance ahead of specific rules.

Can explainable AI eliminate bias in financial models?

No it makes bias easier to detect, not automatically absent. Explanation methods can reveal that a model is relying on a proxy for a protected characteristic, but removing that bias still requires deliberate retraining, feature engineering, or policy changes.

Key Takeaways

Explainable AI in finance has moved from a nice-to-have research topic to a live compliance and business requirement, with the EU AI Act’s August 2026 deadline acting as the clearest forcing function globally. SHAP and LIME remain the workhorse techniques, but neither is infallible, and the smartest teams treat disagreement between explanation methods as useful information rather than noise. The real frontier and the part regulators haven’t caught up to is agentic AI, where the entire premise of feature-attribution explainability starts to break down. Institutions that build tiered, audience-appropriate explanations now, rather than treating XAI as a report generated after the fact, will be far better positioned as both enforcement and technology keep moving faster than the guidance written to govern them.

This article reflects publicly available research and regulatory guidance as of mid-2026. It is intended for general informational purposes and does not constitute legal, compliance, or investment advice; institutions should consult qualified counsel and risk management professionals before making decisions based on AI governance requirements.

Further Reading

- EU AI Act compliance timeline and high-risk obligations for financial institutions

- UK regulators’ approach to AI oversight in financial services (2026)

- Agentic AI governance gap in US banking regulation

- Bibliometric review of explainable AI research in finance

Visit: Aisofting